De Minimis Safe Harbor Election — Complete Guide for Small Businesses

If you're a small business owner, every dollar and every hour counts. That's why the IRS De Minimis Safe Harbor Election is one of the most practical — and underused — tax strategies available. It allows you to immediately expense low-cost business purchases instead of tracking them as fixed assets, saving you time, simplifying your books, and boosting cash flow at tax time.

This guide covers everything you need to know: what the rule is, who qualifies, how to apply it, and how to avoid the most common mistakes. Looking for a quick breakdown? Watch our 5-minute video explainer here.

Get a free quote in 2 minutes with our service estimator tool here!

What are fixed assets?

Fixed assets are long-term, tangible assets used in your business for more than one year. Common examples include:

• Computers, laptops, and tablets

• Office furniture and fixtures

• Machinery and tools

• Vehicles

Unlike cash or inventory (current assets), fixed assets are normally capitalized — meaning they're recorded on your balance sheet and expensed over time through depreciation. The de minimis rule lets you bypass this process entirely for qualifying low-dollar purchases.

Making the de minimis safe harbor election correctly on your return requires getting it right at filing time. Our tax team handles business tax compliance for NC and SC companies. See Our Business Tax Services →

What Is Capitalization — And Why Does It Matter?

Under Generally Accepted Accounting Principles (GAAP), fixed assets are capitalized: recorded on the balance sheet and written off gradually over their useful life through a process called depreciation. Each year you hold the asset, you record a depreciation expense and adjust its book value accordingly.

Example: You buy a $1,200 laptop. Normally, you'd depreciate it over 3–5 years, claiming a portion of the cost each year. With the de minimis safe harbor election, you can deduct the full $1,200 immediately in the year of purchase — as long as it falls under the IRS threshold.

For most small businesses, managing dozens of depreciation schedules is both time-consuming and error-prone. The de minimis election eliminates this burden for small-dollar items.

What Is the IRS De Minimis Safe Harbor Election?

The IRS created the De Minimis Safe Harbor Election to give businesses a simple, compliant way to expense qualifying low-cost tangible property in the year of purchase, rather than capitalizing it. When applied correctly, it:

• Simplifies bookkeeping by eliminating depreciation schedules for small items

• Speeds up deductions, improving cash flow

• Reduces administrative burden at year-end

• Lowers audit risk when documented properly

Who Should Use the De Minimis Rule?

This election is particularly valuable for:

• Small and mid-sized businesses with frequent low-cost equipment purchases

• Asset-heavy companies that regularly replace tools, devices, or furniture

• Inventory-based businesses managing multiple asset categories

• Companies without in-house accounting teams who need to keep processes simple

IRS Thresholds: What Qualifies?

The IRS sets clear per-item (or per-invoice) limits on what qualifies:

Qualifying purchases include: office chairs, desks, printers, laptops, tablets, small tools, and certain software subscriptions classified as tangible property.

How to Apply the De Minimis Election

Using the election is straightforward, but each step matters for compliance:

1. Identify qualifying assets: Confirm each purchase falls at or below your applicable threshold ($2,500 or $5,000).

2. Keep documentation: Retain all invoices and receipts as proof. These are your audit defense.

3. Attach an election statement: Each year, include a De Minimis Safe Harbor Election Statement with your timely filed tax return.

4. Apply consistently: Don't selectively apply the election. Maintain consistent records across all qualifying items.

Important: The IRS does not allow blanket multi-year elections. You must file the election statement annually, every year you wish to use it.

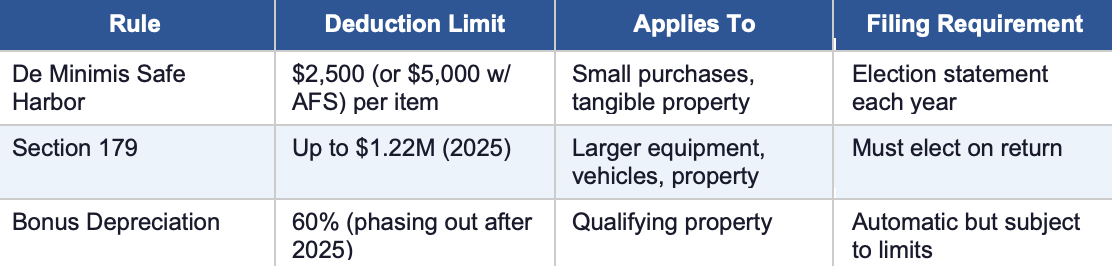

De Minimis vs. Section 179 vs. Bonus Depreciation

The de minimis rule is one of three major deduction strategies for business property. Here's how they compare:

Rule: De Minimis Safe Harbor

Deduction Limit: $2,500 (or $5,000 w/ AFS) per item

Applies To: Small purchases, tangible property

Filing Requirement: Election statement each year

Rule: Section 179

Deduction Limit: Up to $1.22M (2025)

Applies To: Larger equipment, vehicles, property

Filing Requirement: Must elect on return

Rule: Bonus Depreciation

Deduction Limit: 60% (phasing out after 2025)

Applies To: Qualifying property

Filing Requirement: Automatic but subject to limits

Pro Tip: Many small businesses use both De Minimis and Section 179, applying the de minimis election to lower-cost items and Section 179 to larger equipment investments.

Common Mistakes to Avoid

Even experienced business owners run into issues with this election. The most common mistakes we see:

• Forgetting to file the election statement with the tax return each year

• Applying the wrong threshold (e.g., using $5,000 without an AFS)

• Expensing repairs under de minimis when they should be capitalized

• Applying the rule to non-qualifying assets

• Missing documentation — no invoice, no deduction

• Failing to reconcile invoices with fixed asset records

These errors most often surface during audits, tax reviews, or financial cleanups — when they're most costly to correct.

FAQ on De Minimis Safe Harbor Rule:

What is the De Minimis Safe Harbor rule?

It allows businesses to expense certain low-cost items immediately instead of capitalizing them as fixed assets.

What’s the IRS threshold?

$2,500 per invoice/item without audited financials, or $5,000 if your business has an Applicable Financial Statement (AFS).

What qualifies under the rule?

Office supplies, laptops, tablets, printers, small tools, and similar tangible property purchases under the threshold.

How do I make the election?

Attach a De Minimis Safe Harbor Election Statement to your tax return each year. The election must be filed annually — blanket multi-year elections are not allowed.

Does it apply to all businesses?

Yes, but the applicable threshold depends on whether your business has audited financials (AFS).

What is the difference between the De Minimis Election and Section 179?

Section 179 allows larger deductions on qualifying property but has limits; the de minimis election is only for lower-cost items.

Need Help Applying the De Minimis Election?

Certum Solutions specializes in small business accounting, tax compliance, and bookkeeping strategies that maximize deductions.

📅 Book a free 30-minute consultation • 📞 980.210.6946 • ✉️ help@certumsolutions.com

Not sure whether to make the election or how it affects your financials? Our advisory team can walk you through it. Talk to Our Advisors →